March 4, 2026

Why banks still fail at digital engagement (and what needs to change)

For over a decade, banks have invested heavily in mobile apps, digital channels, and customer experience initiatives. Yet, digital engagement remains surprisingly shallow. Banks have built functional channels, but they are mostly optimised for convenience and reassurance rather than meaningful engagement. People log in to check their balance for certainty, the “I’m on top of my money” moment, while apps rarely provide reasons to explore further.

Our own consumer research across several European markets shows a consistent pattern: 80% to 90% of users say the feature they use most is checking their balance. In countries such as Spain, Poland, Greece, and the UK, balance checks lead by a wide margin, followed by confirming deposits or transfers and reviewing recent transactions.

In short, the core digital experience revolves around monitoring money moving in and out of the account. The mobile app has become a transactional utility rather than a meaningful engagement platform that actively supports financial decision-making.

So why, after years of digital transformation, are banks still struggling to move beyond this narrow usage pattern?

The illusion of engagement

From a metrics perspective, daily active users may look healthy, and frequent logins are often interpreted as a sign of strong digital adoption. However, frequency does not necessarily translate into value.

Across the European markets we surveyed, close to half of consumers open their banking app multiple times per day. On paper, this level of habitual usage appears to signal strong engagement.

Yet when viewed alongside the dominant use cases, primarily checking balances and confirming transactions, a different picture emerges. Customers are highly active, but their interactions remain narrow in scope. They return frequently, not because the experience is rich or evolving, but because they feel the need to monitor and verify.

True digital engagement in banking would look very different. It would mean helping customers understand their financial behaviour in context, track meaningful progress towards savings or lifestyle goals, anticipate upcoming financial pressure and receive timely, relevant support without having to search for it.

Despite this, most mobile banking apps remain focused on static information display instead of active financial assistance. They show customers what has happened, but rarely help them understand what it means or what to do next. As a result, the experience remains reactive, and engagement remains superficial.

Raw data without context is not insight

One of the structural reasons behind this gap lies in how financial data is presented. Most mobile banking apps are designed to display transactions efficiently, but not necessarily to interpret them.

Transaction lists, even when categorised, are typically:

- Reactive

- Descriptive rather than interpretative

- Isolated from broader behavioural patterns

Data is displayed, but but rarely translated into actionable insight.

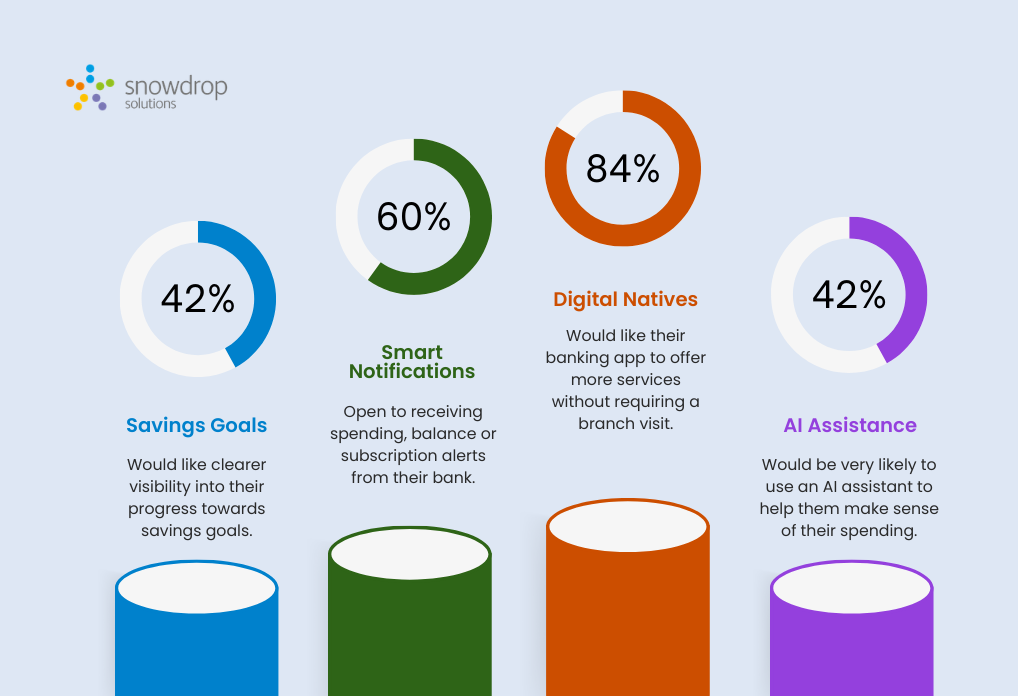

For example, 42% of users say they would like clearer visibility into their progress towards savings goals. It is a request for context, not more data.

Similarly, 60% say they are open to receiving spending, balance or subscription alerts from their bank. This indicates that customers are not resistant to engagement; they are actively inviting it.

The appetite for insight exists. What is missing is the layer of contextual intelligence that transforms raw financial data into something actionable.

Without that layer to explain what the numbers mean, mobile banking just gives you information; it doesn’t really help. And raw information on its own rarely gets people engaged.

Banks lack visibility into the consumer journey

Another fundamental challenge sits beneath the surface of the mobile experience: structure.

Many banks still operate across fragmented systems and product silos, payments, lending, savings, customer support, each functioning efficiently on its own, but rarely orchestrated around a unified customer journey. Without a connected view of behaviour across products and moments, it becomes difficult to deliver interactions that feel timely, relevant or genuinely supportive.

Over time, this design philosophy reinforces a transactional relationship. The bank provides tools; the customer does the work. There is little sense of progression, guidance or continuity across financial decisions. Interactions are initiated by the user and resolved in isolation, rather than forming part of an ongoing, intelligent dialogue.

Yet consumer expectations are shifting. 44% of users say they would like their banking app to offer more services without requiring a branch visit. It signals a desire for the app to become the primary interface for managing financial life, not simply a viewing window into an account.

Without a connected view of behaviour across products and moments, it becomes difficult to deliver interactions that feel timely, relevant or genuinely supportive.

To meet that expectation, banking must evolve beyond utility. It must move from being a passive instrument that records financial activity to an active companion that understands context, anticipates needs and supports decisions over time.

Until that shift happens, digital banking will remain functional, but won’t transform the user experience.

| Feature | Legacy Utility Model | Deep Engagement Model |

|---|---|---|

| Focus | Transactional & reactive | Contextual & anticipatory |

| Data presentation | Descriptive lists | Actionable guidance |

| User intent | Verification (reassurance) | Financial progress & support |

| Bank’s role | Passive record-keeper | Intelligent active companion |

The generational shift: Why expectations are moving faster than banks

Moreover, a further pressure point comes from generational change.

Digital-native institutions such as Monzo and Revolut have not simply introduced new features; they have reshaped expectations around what a banking experience should feel like.

For younger consumers, financial services are evaluated against the standards set by the wider digital economy. In particular, they expect:

- Real-time notifications

- Intuitive categorisation

- Preferences and relevant recommendations

- Visual insights

- Seamless digital journeys

Traditional engagement models, designed around account maintenance rather than behavioural insight, struggle to resonate with this mindset. What once felt secure and reliable can now feel distant and unresponsive.

The competitive landscape has changed. Customer expectations have changed. But many mobile banking experiences have not. The result is a widening gap between how customers experience digital services elsewhere and how they experience their bank.

From traditional banking, displaying only transactions, to smart banking that offers recommendations based on the user’s goals and spending patterns – Created with Stitch for illustrative purposes only, not a real product.

The AI paradox: Investment without transformation

Banks are pouring resources into artificial intelligence. Innovation budgets are rising, AI initiatives are accelerating, and digital roadmaps increasingly feature machine learning capabilities. However, for many customers, the everyday banking experience hasn’t changed much.

The issue is not a lack of technology. It is how that technology is applied.

In many cases, AI is layered on top of legacy engagement models rather than embedded into them. If the core experience remains static, reactive and transaction-focused, no amount of surface-level feature expansion will fundamentally change engagement levels. A smarter notification or a more advanced dashboard does not automatically create a more meaningful relationship.

The real gap is contextual intelligence: the ability to interpret behaviour and translate data into guidance.

Importantly, customers appear ready for that shift. Our research shows strong openness to AI-based assistance in banking. In the UK, 42% of respondents say they would be very likely to use an AI assistant to help them make sense of their spending. Similar trends emerge across Spain, Greece and Poland, where around four in ten consumers express a clear interest in AI-driven support.

This suggests that resistance is not the barrier. Relevance is.

Consumers are not asking for more features; they are asking for clearer understanding. They want help interpreting their financial activity, not just access to it. Until AI is used to transform the experience, rather than decorate it, digital engagement in banking will remain incremental rather than truly intelligent.a

From digital access to daily relevance

Customers are highly active in mobile banking, but engagement often remains limited to checking balances, reviewing transactions and monitoring money movement. To move beyond this, banks need to redefine digital engagement not by usage metrics alone, but by how relevant and supportive the experience is in helping customers make better decisions at the right moment.

This means shifting from static information to contextual, intelligent guidance that fits naturally into everyday financial life. Consumers are already open to proactive alerts, clearer visibility of their financial position and AI-assisted support, signalling a real demand for more responsive banking experiences.

Ultimately, the future of engagement will depend on how well banks can embed context, timing and meaningful interaction into their digital services, making banking feel more connected to customers’ daily financial needs.

Marketing & Comms Director

Seasoned Marcomms professional with 8+ years of experience in brand management and digital communications. I thrive on creating impactful content and creative strategies, leveraging location-enhanced data enrichment insights for financial and digital technology companies. In my spare time, I nurture my mind and spirit through creative pursuits and immersive reading.